AnandTech is out with a rundown on the latest from Intel.

If you're interested in building a database or quant machine with big cujones, the last table on the page gives you the numbers. The quote is $7,080, which is much higher than such a machine would need. You can skip the GPUs (well, at least two of them), drop a couple of hundred watts from the psu, and easily get under $5,000. Running R and any of the open source (or free, as in beer, commercial) databases in 64 gig and 2 terabytes (skip RAID? why not?) of space. That's a couple of weeks of salary for a quant or database dev. Really. You can afford it; the neverending free food'll cost you more.

29 August 2014

28 August 2014

Reservations for ... 8 billion??

Quite recently, in various versions of these endeavors, there was an essay dealing with the Old Gold vs. New Gold situation. Not for the first time.

Imagine my surprise, and wistfulness at not having gotten paid, to see today's NYT piece on just that subject. And about the same conclusion. Well, sort of.

Bernstein paraphrases a Treasury economist (Kenneth Austin) who has published an essay in The Journal of Post Keynesian Economics, here (it's not open, alas). The notion of post Keynes usually means full bore Randian, but not in this case:

In any case, neither Bernstein nor Austin (filtered by Bernstein) defend the notion of the reserve country having to be a net debtor, only that the level of its currency circulating can, more or less, be under its control. As events stand now, they both argue the USofA is at the world's economies' mercy.

The Unfortunate Alternative is hard specie, and one need only read up world, and USofA, economic history from the 19th century through the Great Depression to see how foolish that is. If you think the world is not level now, you ain't seen nuthin yet.

The hidden truth: the country with the reserve currency of the global economy will always, in fact must, run trade deficits. Think about the situation from the point of view of other economies. They have to get reserve currency in order to acquire goods and services.

Imagine my surprise, and wistfulness at not having gotten paid, to see today's NYT piece on just that subject. And about the same conclusion. Well, sort of.

Bernstein paraphrases a Treasury economist (Kenneth Austin) who has published an essay in The Journal of Post Keynesian Economics, here (it's not open, alas). The notion of post Keynes usually means full bore Randian, but not in this case:

Post-Keynesian economists are united in maintaining that Keynes's theory is seriously misrepresented by the two other principal Keynesian schools: neo-Keynesian economics which was orthodox in the 1950s and 60s -- and by New Keynesian economics, which together with various strands of neoclassical economics has been dominant in mainstream macroeconomics since the 1980s.

In any case, neither Bernstein nor Austin (filtered by Bernstein) defend the notion of the reserve country having to be a net debtor, only that the level of its currency circulating can, more or less, be under its control. As events stand now, they both argue the USofA is at the world's economies' mercy.

The Unfortunate Alternative is hard specie, and one need only read up world, and USofA, economic history from the 19th century through the Great Depression to see how foolish that is. If you think the world is not level now, you ain't seen nuthin yet.

24 August 2014

The Poor Will Always Be Us

The environs of Washington, DC are widely excoriated by The Right as being the bastion of Liberal Evil. Not least, the disparity of median income there being higher than most, if not all depending on the year measured, of the rest of the country. Having lived there for the better part of a decade, I can say with certainty that income level was and is driven by the private sector consultants and such, not the bureaucrats who have difficulty keeping up. Bureaucrats aren't living in the big houses in McLean. The academic scene is largely liberal, with the notable exception of George Mason University, in Virginia. That state is really two, with Northern Virginia (actually spelled as such) turning a once deep red state a pleasing shade of lavender. It ain't blue yet, however.

GMU provides the NYT with one of its token right wingnuts, in the person of Tyler Cowen, who regularly displays a breathtaking degree of cognitive dissonance. That the Times would continue to print his stuff is puzzling. I can only guess that the Editors are allowing the loonies to shoot themselves in the foot on full view. I mention this mostly because his essay today exceeds his usual level of incompetence and villainy.

Let's wield the sharp cutlery, shall we?

The overarching theme of the piece is that 18th and 19th century India is prescriptive for today's US and Western economies generally. Baloney. The 18th and 19th century global economy was dominated by mercantilism, with India and the New World colonies being principle examples of those on the losing end of the bargain. This period was marked, more than any other way, by the discovery and pillaging of natural resources in this New World, mostly by European overseers. The second most important point was the development of science and engineering from primitive to near completion (save for Einstein and Bohr and the final entries in the periodic table). Most of the widgets that you use and prize today were invented by The Great Depression, they're just smaller and faster now. In other words: the scope of new knowledge and new resources from 1800 to 1900 overwhelms what can be expected from 2000 forward. The simple fact is, we know just about all there is to know about the physical world and where the useful parts reside. And there is no New World to pillage. (For those talking about mining other planets and such: not with chemical rockets, boyo.) And we're nearing, if not met, the carrying capacity of these, now firmly limited, resources. Wealthy Chinese are scuttling away from their air and water as fast as possible. The notion that there's some magical, as yet undiscovered, venue of employment to support a vast new middle class is a pipe dream (and that phrase refers to the Chinese opium pipe, just so you know). The journey goes from farm to factory to cubicle. Full stop. We've found the whole pie, now we need to carve it up in such a way that civilization survives.

Well, let's consider this period. Slave based production of cotton and textiles by the US South dominated the period. Why ship cotton half way around the world, when your slaves can grow it here? Of course, not. Virginia (tobacco) and the Carolinas (rice and cotton) are much closer to London than anywhere in India, after all. At the time of the American Revolution, slavery production was the major source of hard currency, not manufacturing. India didn't stand a chance. Moreover, industrializing agriculture yields more poor people when there aren't alternatives. Take the modern example: robotics replacing hands in the manufacture of autos. You know the rest. The notion that India somehow missed its opportunity to be Europe's supplier of industrial output in 1850, or thereabouts, if only India had spent more on machines is asinine. The reason that Apple, and the rest, can exploit China is the 747 freighter. That aircraft didn't exist in 1850. Nor did the container ship.

Here's where the cognitive dissonance really kicks in:

The post WWII economic surge was built on the afterglow of socialism, but not by that name, of course. The war effort was a case of "all for one, and one for all". The notion of shared responsibility, rather than Randian greed (she didn't start in earnest until the 1950s), was the order of the day. Corporations paid real taxes, unions bargained widely, and Bretton Woods made the US buck supreme. Cowen, either because he's too stupid or vile, elides the simple fact: American corporations now exploit totalitarian labor for the benefit of the few. It was brought to you by Richard Nixon in 1972.

But this is all good for China, right?

Well, Cowen, being an econ professor, knows that even in the best of economies mean/average/per capita income overstates reality. I can't find a median income measure for China, but that's not too surprising:

(The US gini, 2011, was .477. That's worse than China, just to be clear how the number works.)

China's .1% are doing just fine, thanks. The rest, not so much.

I wonder, how did per capita income quintuple in a year? It didn't of course. Cowen just made it up. Or the ghost of Ayn whispered it in his ear while he nodded off during a lecture at AEI.

Back to Cowen:

So, it would appear, Cowen's remedy is for Western labor to accept Eastern poverty as the new normal? How, exactly, is that progress or a solution?

Reading history, and data, makes the story quite clear. Economies which (ahem!) enforce equity, such as the Scandinavians, thrive overall, while those which embrace Rand fall into revolt. Cowen bemoans the prospect of stagnant/falling median income in the USofA, but at no point offers a remedy other than benign acceptance; it's God's will. He has to know that while median income has gotten poorer, the 1% have gotten richer. And he has to know that these effects derive in concert, not by coincidence. And he has to know that slack demand is the result. And that slack demand leads to lowering median income. Rinse. Repeat.

When the dominance of a service economy was being first recognized, in the 1970s, the notion was that such a move was at least as beneficial, overall, as the migration from farm to factory pre-WWII. Instead of factory workers, we'd all be office think workers, earning much more than our beaten down factory fathers. Hasn't worked out that way. We, still, mostly buy real widgets. You can't eat software.

We can't all be London Whales, crashing our small corner of the economy. And if we were, the whole economy crashes. Wait, didn't we do that?

So, you can be poor because totalitarian regimes elsewhere keep wages at bare subsistence and your job goes there or... you can be poor here as corporations implement wage arbitrage down to bare subsistence with the outsourcing as threat. Of course, in due course, there'll be no one in the USofA, or anywhere else, who can buy the all the widgets being made. What a country!! The United States of Mississippi. But, of course, you can't sell much in Mississippi; they're all really, really poor.

The fundamental problem is that wage or tax or foo arbitrage by corporations ultimately fails for structural reasons. As your Good Mother told you, "what would the world be like, if everybody behaved like you?" The second and third worlds, largely autocratic governments, provide cheap hands in order to earn hard currency (which they, mostly, keep for themselves, of course). Today, that's the US buck. The same thing goes on here, the red states ban unions and drive down wages, so corporations move to such states. The problem, of course, is that both kinds of arbitrage depend, absolutely, on a high wage population (those God hating blue staters, of course) to suck up output. What happens when there's no longer a pool of high wage earners to export to? The issue grows more dire as automation becomes both more widespread and expensive. You do remember the story about ditching 300mm wafer production for 450mm?? Hasn't happened. Likely, never will; insufficient demand for so many more chips to pay for the machinery. In due course, and since the world is non-linear (according to Dr. McElhone), demand utterly collapses when least expected.

GMU provides the NYT with one of its token right wingnuts, in the person of Tyler Cowen, who regularly displays a breathtaking degree of cognitive dissonance. That the Times would continue to print his stuff is puzzling. I can only guess that the Editors are allowing the loonies to shoot themselves in the foot on full view. I mention this mostly because his essay today exceeds his usual level of incompetence and villainy.

Let's wield the sharp cutlery, shall we?

For all the talk of the Great Depression, we might look at a different exemplar for modern times, 18th- and 19th-century economic history India. That country's economic retrogression during that era may help us understand the quandary that some parts of the world face today.

The overarching theme of the piece is that 18th and 19th century India is prescriptive for today's US and Western economies generally. Baloney. The 18th and 19th century global economy was dominated by mercantilism, with India and the New World colonies being principle examples of those on the losing end of the bargain. This period was marked, more than any other way, by the discovery and pillaging of natural resources in this New World, mostly by European overseers. The second most important point was the development of science and engineering from primitive to near completion (save for Einstein and Bohr and the final entries in the periodic table). Most of the widgets that you use and prize today were invented by The Great Depression, they're just smaller and faster now. In other words: the scope of new knowledge and new resources from 1800 to 1900 overwhelms what can be expected from 2000 forward. The simple fact is, we know just about all there is to know about the physical world and where the useful parts reside. And there is no New World to pillage. (For those talking about mining other planets and such: not with chemical rockets, boyo.) And we're nearing, if not met, the carrying capacity of these, now firmly limited, resources. Wealthy Chinese are scuttling away from their air and water as fast as possible. The notion that there's some magical, as yet undiscovered, venue of employment to support a vast new middle class is a pipe dream (and that phrase refers to the Chinese opium pipe, just so you know). The journey goes from farm to factory to cubicle. Full stop. We've found the whole pie, now we need to carve it up in such a way that civilization survives.

In 1750, India accounted for one-quarter of the world's manufacturing output, but by 1900 that was down to 2 percent.

...

India just didn't do enough to move toward production on a larger scale or with better machines.

Well, let's consider this period. Slave based production of cotton and textiles by the US South dominated the period. Why ship cotton half way around the world, when your slaves can grow it here? Of course, not. Virginia (tobacco) and the Carolinas (rice and cotton) are much closer to London than anywhere in India, after all. At the time of the American Revolution, slavery production was the major source of hard currency, not manufacturing. India didn't stand a chance. Moreover, industrializing agriculture yields more poor people when there aren't alternatives. Take the modern example: robotics replacing hands in the manufacture of autos. You know the rest. The notion that India somehow missed its opportunity to be Europe's supplier of industrial output in 1850, or thereabouts, if only India had spent more on machines is asinine. The reason that Apple, and the rest, can exploit China is the 747 freighter. That aircraft didn't exist in 1850. Nor did the container ship.

Here's where the cognitive dissonance really kicks in:

International trade grew rapidly after World War II, but at least in the early postwar years most of that trade was among countries with roughly comparable technologies and real wages. And that trade spurred growth rather than damaging laggard economies.

In the last 20 years, the economic surge of Asia, especially China, has brought a large trade readjustment to the world, one with few parallels with the possible exception of the rise of the Western economies several centuries ago.

The post WWII economic surge was built on the afterglow of socialism, but not by that name, of course. The war effort was a case of "all for one, and one for all". The notion of shared responsibility, rather than Randian greed (she didn't start in earnest until the 1950s), was the order of the day. Corporations paid real taxes, unions bargained widely, and Bretton Woods made the US buck supreme. Cowen, either because he's too stupid or vile, elides the simple fact: American corporations now exploit totalitarian labor for the benefit of the few. It was brought to you by Richard Nixon in 1972.

But this is all good for China, right?

China's per capita income, less than $300 in 1984, is now in the range of $10,000.

Well, Cowen, being an econ professor, knows that even in the best of economies mean/average/per capita income overstates reality. I can't find a median income measure for China, but that's not too surprising:

Results of a wide-ranging survey of Chinese family wealth and living habits released this week by Peking University show a wide gap in income between the nation's top earners and those at the bottom, and a vast difference between earners in top-tier coastal cities and those in interior provinces.

...

In March 2012, Bo Xilai, a top party official who was trying to create a populist image for himself and was later purged, said at a news conference that the Gini coefficient had reached an alarming 0.46. His willingness to announce the number came as a surprise to many observers.

(The US gini, 2011, was .477. That's worse than China, just to be clear how the number works.)

China's .1% are doing just fine, thanks. The rest, not so much.

Average annual income for a family in 2012 was 13,000 renminbi, or about $2,100.

I wonder, how did per capita income quintuple in a year? It didn't of course. Cowen just made it up. Or the ghost of Ayn whispered it in his ear while he nodded off during a lecture at AEI.

Back to Cowen:

French citizens expect a great deal from their government, and strikes are a common response to reduced wages or benefits.

...

Chinese export growth and wage competition may have been a kind of final straw that made old ways unsustainable.

So, it would appear, Cowen's remedy is for Western labor to accept Eastern poverty as the new normal? How, exactly, is that progress or a solution?

Reading history, and data, makes the story quite clear. Economies which (ahem!) enforce equity, such as the Scandinavians, thrive overall, while those which embrace Rand fall into revolt. Cowen bemoans the prospect of stagnant/falling median income in the USofA, but at no point offers a remedy other than benign acceptance; it's God's will. He has to know that while median income has gotten poorer, the 1% have gotten richer. And he has to know that these effects derive in concert, not by coincidence. And he has to know that slack demand is the result. And that slack demand leads to lowering median income. Rinse. Repeat.

When the dominance of a service economy was being first recognized, in the 1970s, the notion was that such a move was at least as beneficial, overall, as the migration from farm to factory pre-WWII. Instead of factory workers, we'd all be office think workers, earning much more than our beaten down factory fathers. Hasn't worked out that way. We, still, mostly buy real widgets. You can't eat software.

We can't all be London Whales, crashing our small corner of the economy. And if we were, the whole economy crashes. Wait, didn't we do that?

So, you can be poor because totalitarian regimes elsewhere keep wages at bare subsistence and your job goes there or... you can be poor here as corporations implement wage arbitrage down to bare subsistence with the outsourcing as threat. Of course, in due course, there'll be no one in the USofA, or anywhere else, who can buy the all the widgets being made. What a country!! The United States of Mississippi. But, of course, you can't sell much in Mississippi; they're all really, really poor.

The fundamental problem is that wage or tax or foo arbitrage by corporations ultimately fails for structural reasons. As your Good Mother told you, "what would the world be like, if everybody behaved like you?" The second and third worlds, largely autocratic governments, provide cheap hands in order to earn hard currency (which they, mostly, keep for themselves, of course). Today, that's the US buck. The same thing goes on here, the red states ban unions and drive down wages, so corporations move to such states. The problem, of course, is that both kinds of arbitrage depend, absolutely, on a high wage population (those God hating blue staters, of course) to suck up output. What happens when there's no longer a pool of high wage earners to export to? The issue grows more dire as automation becomes both more widespread and expensive. You do remember the story about ditching 300mm wafer production for 450mm?? Hasn't happened. Likely, never will; insufficient demand for so many more chips to pay for the machinery. In due course, and since the world is non-linear (according to Dr. McElhone), demand utterly collapses when least expected.

23 August 2014

Am I Blue? Yes, I Am

While I dearly love DB2 on LUW, I've been putting off upgrading the editor needed for 10.x. Prior, the Control Center was very easy to use and not too much of an install. This newfangled "Data Studio" is 1.5 gig of download and a java/eclipse beast. A DSL killer. Well turns out, there's a way to get it without using the on-line Install Manager. This post lays it out. One point of confusion is that the repository adding happens off the initial File menu; I spent a couple of times fighting with on-line nonsense. Just fire up the download when Olbermann comes on, go to sleepy sleep, and wake up with a huge gzipped tar file. Talk about bloat?

Still can't, that I've found, use it with PG, of course. Offers up MySql, along with the usual commercial suspects. DB2 has so many dials and knobs in the engine that one can tune (and that none of the others, especially OS, have), that multi-database editors such as AQT and Aqua (haven't used Toad in a while, so I can't say) don't bother to add support for such a small market share database. Too bad about that part, since DB2 really rocks.

Still can't, that I've found, use it with PG, of course. Offers up MySql, along with the usual commercial suspects. DB2 has so many dials and knobs in the engine that one can tune (and that none of the others, especially OS, have), that multi-database editors such as AQT and Aqua (haven't used Toad in a while, so I can't say) don't bother to add support for such a small market share database. Too bad about that part, since DB2 really rocks.

20 August 2014

Danger Will Robinson, Again

simple-talk has an interview with Bjarne Stroustrop just up. It's a better interview than most, by the way. Well worth the effort. Reading it reminded me of a quote from Stroustrop, but for which I cannot vouch, since I've long lost the cite. I've been looking to confirm it for years.

It may be C++. And it may never have been said by him. Or anyone. The Voices may have just assimilated me.

Anyway, the interview has me off looking, again. I did find this piece, which provides the quote which got me into so much trouble with the Indians at CSC:

Organic length of code, as organic normal form, is the ideal to be sought. The fascination with two or three line methods, tens or dozens of 'em, means only one thing: in order to understand the functioning of the object, one has to hold lots of stuff in one's immediate memory. Few can do that, so most OO code ends up being written in the (GUI) debugger. Unlike the Deming Dance (do it right the first time), this is pound the hammer until you bust the thing to pieces.

Not to mention the corrosive effect of the web: OOD/OOP has devolved back to function/data of FORTRAN, only we now adopt the terms ActionObject and DataObject. As Stein said about Oakland, "there's no there, there". OOD/OOP means that objects really are self-contained, and communicate with other objects with messages (which is to say, "do something, and I don't care how"), not data packets. Where did I park that DeLorean??

Object oriented programming is buzzword programming.

It may be C++. And it may never have been said by him. Or anyone. The Voices may have just assimilated me.

Anyway, the interview has me off looking, again. I did find this piece, which provides the quote which got me into so much trouble with the Indians at CSC:

As we have all learned, methods in good OO programs should be short and sweet. Lots of little methods are good for development, understanding, reuse, and so on. Well, what's the problem with that?

Well, consider that we actually spend more time reading OO code than writing it. This is what is known as productivity. Instead of spending many hours writing a lot of code to add some new functionality, we only have to write a few lines of code to get the new functionality in there, but we spend many hours trying to figure out which few lines of code to write!

One of the reasons it takes us so long is that we spend much of our time bouncing back and forth between ... lots of little methods.

This is sometimes known as the Lost in Space syndrome. It has been reported since the early days of OOP. To quote Adele Goldberg, "In Smalltalk, everything happens somewhere else."

Organic length of code, as organic normal form, is the ideal to be sought. The fascination with two or three line methods, tens or dozens of 'em, means only one thing: in order to understand the functioning of the object, one has to hold lots of stuff in one's immediate memory. Few can do that, so most OO code ends up being written in the (GUI) debugger. Unlike the Deming Dance (do it right the first time), this is pound the hammer until you bust the thing to pieces.

Not to mention the corrosive effect of the web: OOD/OOP has devolved back to function/data of FORTRAN, only we now adopt the terms ActionObject and DataObject. As Stein said about Oakland, "there's no there, there". OOD/OOP means that objects really are self-contained, and communicate with other objects with messages (which is to say, "do something, and I don't care how"), not data packets. Where did I park that DeLorean??

18 August 2014

Life is A Totem Pole

Having lived, in my first job in Boston and thence in Washington, DC (and having done my grad school in econometrics), the notion of localized inflation was well understood at least as far back as the 1970s. No matter where you work/live, the $$$ you get paid aren't what determine how well you live, but where those $$$ seat you on the local totem pole. I guess it's still news to some folks.

Interception

These endeavors have spent a lot of virtual ink over the last year or so making that case that financial quants don't know as much as they think, and that the events which led to The Great Recession and London Whale should be, but clearly haven't been, teaching moments. I've heard tell of various bots and such, but this expose` is truly mindnumbing.

As has been promulgated here, it is events which move data, not the other way 'round. While time series analysis can give one a warm and fuzzy feeling that the way of the world is clearly delineated in all-the-data-to-today, and one can happily predict off the end of this curve, it's not much more than tossing a dart in a pub.

You must read it.

As has been promulgated here, it is events which move data, not the other way 'round. While time series analysis can give one a warm and fuzzy feeling that the way of the world is clearly delineated in all-the-data-to-today, and one can happily predict off the end of this curve, it's not much more than tossing a dart in a pub.

You must read it.

17 August 2014

An Open Letter to Dr. Shiller [update]

In today's Times Business section, Robert Shiller gives his take on stocks, specifically the question: are they priced too high? He titles the piece (dead trees version), "The Mystery of Lofty Elevations". The web title is similar.

Note, of course the use of the word 'mystery'. Are stock prices really too high? As I've been arguing for some time, NO. Those with piles of moolah to 'invest' have traditionally been in bonds, clipping coupons each quarter. Living off the interest, in simple terms. As even Dr. Shiller has to know, short term interest rates (in particular, the Fed Funds rate) are not what determines long term (corporate) interest rates. The value of corporate bonds is determined by the return earnable from new plant and equipment in the hands of 'job creators'. To the extent that 'job creators' choose to not buy plant and equipment, at any rate of interest, then the long term return to moolah holders will go down.

There's also the matter of the supply of loanable funds, aka "The Giant Pool of Money". It's still around, and corporations continue to hold ever larger amounts of idle cash. They'd love, I'm sure, to be given 10% annually by Washington or Bejing, but that ain't gonna happen. Until such time as the 'job creators' decide that physical investment is more lucrative than fiduciary games, the supply of long term funds will outstrip the demand for such. It's that simple. So far, their notion of smart capital allocation is to stuff it into the mattress.

The Captains of Industry have simply run out of ideas. The digital economy is, on the whole, super-cheap to run. Even as we approach the next (and, perhaps, last) barrier to continuance of Moore's Law (for myself, it looks like physics has repealed the law), the cost per cycle continues to diminish. In any case, the web economy amounts to little more than giants and dwarves fighting over advert buyers and advert clickers. Arabs, and their blue eyed Texas brethren, learned the hard way that you can't eat oil. The web economy will eventually realize that advert peddling is just a lot of wheel spinning; much ado about little.

It's as simple as I've said: bond prices are high (yields low) because the Captains of Industry aren't smart enough to figure out new ways to turn moolah into machines. Even with money available at historically low rates, and retained earnings at historical highs, the Captains just don't know what to do with it.

And, in other words, all those Koch Brothers types who bleat that Americans have to save and invest more ignore the plain fact that corporate America hasn't been able to allocate The Giant Pool of Money that's already sloshing around. Push more money into the Pool, and returns will fall still further. Econ 101.

We can expect yet more bleating from the .1% class that capital gains taxes are ruinous. Why? Since they can't get by on the low coupon returns, they must needs turn to stock price appreciation (as we've seen) and share selling for income. And, of course, since only Little People pay taxes, their incomes shouldn't be taxed. Just watch.

[update]

Seems some of the sell-side analysts (larger fish in the pundit pond than I, alas) take exception. This shouldn't be too surprising, since they make their obscene incomes flogging stocks. But they do have a salient point: they tout forward P/E, while Shiller's CAPE (where's Superman when you need him) is explicitly backward looking and for a long time at that. The notion that more data is better is generally a good thing, except when there's been an inflection in the data of your model, and worse if the inflection is in the recent past. The evidence is clear that the Captains of Industry are using fiduciary capital in more financial engineering exercises and less in buying plant and machines. No physical investment, no hard returns to capital, no interest earned, no demand for additional capital. The causation is that long term earnings determine short term rates. Central banks can hope to manipulate short term rates, and even set one or two, but they can't change the course of science and engineering (the real kind). Without tech progress, there's only foregone consumption to pay the vig. Looking at 21st century economies through the lens of 19th century experience (even to mid 20th) is folly.

It isn't a fluke that The Giant Pool of Money (larger now than then) was dumped into non-productive real estate. The Captains of Industry had no use for it. They still don't.

Note, of course the use of the word 'mystery'. Are stock prices really too high? As I've been arguing for some time, NO. Those with piles of moolah to 'invest' have traditionally been in bonds, clipping coupons each quarter. Living off the interest, in simple terms. As even Dr. Shiller has to know, short term interest rates (in particular, the Fed Funds rate) are not what determines long term (corporate) interest rates. The value of corporate bonds is determined by the return earnable from new plant and equipment in the hands of 'job creators'. To the extent that 'job creators' choose to not buy plant and equipment, at any rate of interest, then the long term return to moolah holders will go down.

There's also the matter of the supply of loanable funds, aka "The Giant Pool of Money". It's still around, and corporations continue to hold ever larger amounts of idle cash. They'd love, I'm sure, to be given 10% annually by Washington or Bejing, but that ain't gonna happen. Until such time as the 'job creators' decide that physical investment is more lucrative than fiduciary games, the supply of long term funds will outstrip the demand for such. It's that simple. So far, their notion of smart capital allocation is to stuff it into the mattress.

The Captains of Industry have simply run out of ideas. The digital economy is, on the whole, super-cheap to run. Even as we approach the next (and, perhaps, last) barrier to continuance of Moore's Law (for myself, it looks like physics has repealed the law), the cost per cycle continues to diminish. In any case, the web economy amounts to little more than giants and dwarves fighting over advert buyers and advert clickers. Arabs, and their blue eyed Texas brethren, learned the hard way that you can't eat oil. The web economy will eventually realize that advert peddling is just a lot of wheel spinning; much ado about little.

So I've been trying to come up with a theory to explain today's elevated stock prices -- and maybe convince myself that they could remain lofty for some time. One factor to consider is that bond prices are high, too.

It's as simple as I've said: bond prices are high (yields low) because the Captains of Industry aren't smart enough to figure out new ways to turn moolah into machines. Even with money available at historically low rates, and retained earnings at historical highs, the Captains just don't know what to do with it.

When there aren't enough good investing opportunities, people wishing to save more for the future may succeed only in bidding up existing assets even if they think they're overpriced. Call it the "life preserver on the Titanic" theory.

And, in other words, all those Koch Brothers types who bleat that Americans have to save and invest more ignore the plain fact that corporate America hasn't been able to allocate The Giant Pool of Money that's already sloshing around. Push more money into the Pool, and returns will fall still further. Econ 101.

We can expect yet more bleating from the .1% class that capital gains taxes are ruinous. Why? Since they can't get by on the low coupon returns, they must needs turn to stock price appreciation (as we've seen) and share selling for income. And, of course, since only Little People pay taxes, their incomes shouldn't be taxed. Just watch.

[update]

Seems some of the sell-side analysts (larger fish in the pundit pond than I, alas) take exception. This shouldn't be too surprising, since they make their obscene incomes flogging stocks. But they do have a salient point: they tout forward P/E, while Shiller's CAPE (where's Superman when you need him) is explicitly backward looking and for a long time at that. The notion that more data is better is generally a good thing, except when there's been an inflection in the data of your model, and worse if the inflection is in the recent past. The evidence is clear that the Captains of Industry are using fiduciary capital in more financial engineering exercises and less in buying plant and machines. No physical investment, no hard returns to capital, no interest earned, no demand for additional capital. The causation is that long term earnings determine short term rates. Central banks can hope to manipulate short term rates, and even set one or two, but they can't change the course of science and engineering (the real kind). Without tech progress, there's only foregone consumption to pay the vig. Looking at 21st century economies through the lens of 19th century experience (even to mid 20th) is folly.

It isn't a fluke that The Giant Pool of Money (larger now than then) was dumped into non-productive real estate. The Captains of Industry had no use for it. They still don't.

13 August 2014

DBA According to Moses

Every now and again I'll run across a posting which is prescriptive in nature. Some more aggressive in tone than others. Today brings a latter day Moses, via the PG site.

I didn't add anything, or more commandments. What piques my interest, enough to spend a few minutes typing, is the nature of his commandments. Fact is, that's always the interesting bit to such posts: what is the battlefield?

For a database oriented site, it was, at one time, about a 50/50 chance that the battlefield was over how to build database-centric applications in the face COBOL/PHP/java + RBAR data opposition. Alas, these days it seems that even the simple-talk, and certainly the PG folks (it is a code + RBAR oriented datastore from the beginning), have been assimilated by the Borg. It's really too bad. Current technology, modulo the Big Data knuckleheads, is exactly what Dr. Codd had in mind when laying out the RM: all is related, all actions happen "at once", and implmentation is left to the vendor. The key notion to the RM, more than any other aspect, is analogous to the difference between sigma notation and matrix notation. RBAR on the one hand, and it-happens-all-at-once on the other. Of course, real hardware is inherently sequential on the metal. Well, in truth, not so much any longer.

Anyway, this Moses posting is about the care and feeding aspects, what was once the only definition, of DBA. Save for a jibe to promote better coding!! Too bad. Dr. Codd's ghost should be haunting more who claim to "do" RDBMS. May be then we'll all find the gonads to fight for what is right? We need a Bravedata, complete with lots o blue paint (that's IBM avatar, of course).

I didn't add anything, or more commandments. What piques my interest, enough to spend a few minutes typing, is the nature of his commandments. Fact is, that's always the interesting bit to such posts: what is the battlefield?

For a database oriented site, it was, at one time, about a 50/50 chance that the battlefield was over how to build database-centric applications in the face COBOL/PHP/java + RBAR data opposition. Alas, these days it seems that even the simple-talk, and certainly the PG folks (it is a code + RBAR oriented datastore from the beginning), have been assimilated by the Borg. It's really too bad. Current technology, modulo the Big Data knuckleheads, is exactly what Dr. Codd had in mind when laying out the RM: all is related, all actions happen "at once", and implmentation is left to the vendor. The key notion to the RM, more than any other aspect, is analogous to the difference between sigma notation and matrix notation. RBAR on the one hand, and it-happens-all-at-once on the other. Of course, real hardware is inherently sequential on the metal. Well, in truth, not so much any longer.

Anyway, this Moses posting is about the care and feeding aspects, what was once the only definition, of DBA. Save for a jibe to promote better coding!! Too bad. Dr. Codd's ghost should be haunting more who claim to "do" RDBMS. May be then we'll all find the gonads to fight for what is right? We need a Bravedata, complete with lots o blue paint (that's IBM avatar, of course).

11 August 2014

A Visit in the Hadleyverse

Hadley Wickham is interviewed by Eduardo Arino de la Rubia in conjunction with the useR! meeting in Los Angeles. He warms the cockles of my heart starting at 15:50 of the interview, when they discuss the bipolar (my term, not theirs) nature of R. Yes, R is both an Excel on steroids (neither of them says Excel, but reading between the lines...) and a kinda, sorta language to write programs. Since most of us know Hadley via his packages (and he's using Rcpp more, lately), and this interview is about how he goes about making same, it's impossible to judge how he feels about R as a stat command language for stats, quants, data scientists, and the like. But it is clear that he gets the difference. It's also my inference that he envisions lots o London Whales making their mistakes in R rather than Excel. Whether that's a good thing is another matter. Sometimes brain surgery should only be done by trained neurosurgeons. If The Great Recession taught us nothing else, it's that quant is too often done cavalierly, by those with little to no understanding of what they're doing, yet with an outcomes' agenda. Bad dog.

07 August 2014

Sovaldi Sings Iago

For those who aren't up on Shakespeare and Rossini, Iago is a bad guy. A really bad guy. Sovaldi, according to some (and a growing count, by most accounts), is the archetype of Big Pharma profiteering; taking money from the many to give to the few for little or no real value.

Sovaldi is Gilead's hep/C vaccine, more accurately anti-viral, which costs $1,000/pill or $84,000/treatment. It is claimed to offer higher cure rate, lower side effects, and shorter treatment period.

Unlike breast cancer or prostate cancer, hep/C, by and large, is a Bad Person's Disease; mostly IV drug users. A lifestyle choice. Mostly, not all. It happens that a large number of the infected are also incarcerated, which shouldn't be too surprising. Turns out prisons don't get mandated discounts. Remember those TV cop shows, where the perp turns out to be an ex-con who just can't seem to get it together on the outside, and heists a bodega in order to get back inside? Likely see more of that.

In other words, this is what happens when public health problems are shunted off to for-profit outfits. Gilead gets all the profit (they did drop more than $11 billion to buy the company which devised it, though). Taxpayers get all the costs. What would Adam Smith (the real one) say? I mean, where's the cost/benefit analysis of making life more comfortable for drug addicts? There are nearly as effective, far less costly, existing therapies. So, what is the marginal benefit? What is the marginal cost?

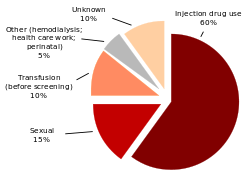

Here's another case where even the 1% will need Obamacare. If the insurance companies, and other right wing scolds ("$84,000 for drug addicts!!") get their way, then far fewer treatments will happen, and Gilead will, unless stopped by the Damn Gummint, raise the price further. By restricting the use of Sovaldi to those who get hep/C, but not through Bad Behavior, the unit price will have to go up in order to preserve Gilead's entitled profit. How much up? Well, according to this chart from CDC data between 5% and 15% of infections can be considered non-willful. Like that word? Very Biblical, that word. So, the innocents infected will have to pay (or some form of insurer) some multiple of $84,000 to keep Gilead in golden threads. Take away 90% of your customers, and, if you can get away with it, the remaining 10% get truly hosed.

Here's the kicker (which hasn't been stated, so far as I've seen): since 60% (more or less) of those infected are IV drug users, and Sovaldi isn't a vaccine which offers immunity to disease, but an anti-viral, we should expect that those 60% will rotate through with some frequency. Drug use: the gift that keeps on giving. Perhaps, at the end of treatment, patients get an 'S' tattoo, indicating that they've had their once-in-a-lifetime Sovaldi treatment. No second helpings.

This is the prototypical case where an army of forensic accountants could be unleashed to discover how much of Sovaldi's claimed development cost actually was spent on the ground, and how much went to SG&A. I'd love to see that number. Not going to happen.

Sovaldi is Gilead's hep/C vaccine, more accurately anti-viral, which costs $1,000/pill or $84,000/treatment. It is claimed to offer higher cure rate, lower side effects, and shorter treatment period.

Unlike breast cancer or prostate cancer, hep/C, by and large, is a Bad Person's Disease; mostly IV drug users. A lifestyle choice. Mostly, not all. It happens that a large number of the infected are also incarcerated, which shouldn't be too surprising. Turns out prisons don't get mandated discounts. Remember those TV cop shows, where the perp turns out to be an ex-con who just can't seem to get it together on the outside, and heists a bodega in order to get back inside? Likely see more of that.

The drug's virtue, that it frequently cures a chronic and sometimes very costly disease, is not always relevant in the prison setting. Hepatitis C can take up to 30 years to turn from active infection to serious liver disease. Therefore, a costly investment in a cure for those prisoners close to their release date will offer no relief to a prison's long-term medical budget, even if it might improve the prisoner's lifetime health.

In other words, this is what happens when public health problems are shunted off to for-profit outfits. Gilead gets all the profit (they did drop more than $11 billion to buy the company which devised it, though). Taxpayers get all the costs. What would Adam Smith (the real one) say? I mean, where's the cost/benefit analysis of making life more comfortable for drug addicts? There are nearly as effective, far less costly, existing therapies. So, what is the marginal benefit? What is the marginal cost?

Here's another case where even the 1% will need Obamacare. If the insurance companies, and other right wing scolds ("$84,000 for drug addicts!!") get their way, then far fewer treatments will happen, and Gilead will, unless stopped by the Damn Gummint, raise the price further. By restricting the use of Sovaldi to those who get hep/C, but not through Bad Behavior, the unit price will have to go up in order to preserve Gilead's entitled profit. How much up? Well, according to this chart from CDC data between 5% and 15% of infections can be considered non-willful. Like that word? Very Biblical, that word. So, the innocents infected will have to pay (or some form of insurer) some multiple of $84,000 to keep Gilead in golden threads. Take away 90% of your customers, and, if you can get away with it, the remaining 10% get truly hosed.

{kind=link}

Here's the kicker (which hasn't been stated, so far as I've seen): since 60% (more or less) of those infected are IV drug users, and Sovaldi isn't a vaccine which offers immunity to disease, but an anti-viral, we should expect that those 60% will rotate through with some frequency. Drug use: the gift that keeps on giving. Perhaps, at the end of treatment, patients get an 'S' tattoo, indicating that they've had their once-in-a-lifetime Sovaldi treatment. No second helpings.

This is the prototypical case where an army of forensic accountants could be unleashed to discover how much of Sovaldi's claimed development cost actually was spent on the ground, and how much went to SG&A. I'd love to see that number. Not going to happen.

06 August 2014

Big Fish, Little Fish

The NYT DealB%k has an interesting piece from one of the regulars on the Big Fish eating the Little Fish in the cloistered world of the innterTubes. But Solomon leaves out the lede, as they say in the pubbiz: these Big Fish ain't really conglomerates.

What he misses, or simply doesn't want to say, is that Google, et al, of today aren't (structurally) anything like GTE, ITT or the rightfully infamous Gulf+Western of Charley Bluhdorn. Those were real conglomerates, with real divisions (ex-companies) in real, different, businesses. With the possible exception (too soon to tell) of Apple/Beats, the rest are all agglomerations of advert pushing platforms. Despite the appearance of differing users and "products" for those users, the real clients are the advert buyers. And they're (Google, et al) all attempting what the New York Yankees have done for generations: buy up any player who's any good to keep said player from ending up with another team. It takes very little to create an web-based advert platform; WhatsApp was, what, 6 guys? If you're Google, that makes your sphincter kinda tight. 93% of its revenue is from adverts, still (last 10-K). How much of its profit is assigned, I couldn't find, but I'll guess all of it. All of the side projects are just that: on the side.

In any case, these aren't conglomerates, just oligopolists aiming to be the monopolist.

The paradox is that conglomerates outside the tech sector are an endangered species. The 1960s was the age of the conglomerates. ITT, for example, made both weapons and movies, with the idea that smart managers could operate any business and different operations would diversify the business. But that strategy did not work out as planned. The problem was that managers needed to focus on their businesses. If investors wanted to diversify, they could do so by simply investing in the separate companies. And splitting off businesses would discipline managers not to waste extra cash.

What he misses, or simply doesn't want to say, is that Google, et al, of today aren't (structurally) anything like GTE, ITT or the rightfully infamous Gulf+Western of Charley Bluhdorn. Those were real conglomerates, with real divisions (ex-companies) in real, different, businesses. With the possible exception (too soon to tell) of Apple/Beats, the rest are all agglomerations of advert pushing platforms. Despite the appearance of differing users and "products" for those users, the real clients are the advert buyers. And they're (Google, et al) all attempting what the New York Yankees have done for generations: buy up any player who's any good to keep said player from ending up with another team. It takes very little to create an web-based advert platform; WhatsApp was, what, 6 guys? If you're Google, that makes your sphincter kinda tight. 93% of its revenue is from adverts, still (last 10-K). How much of its profit is assigned, I couldn't find, but I'll guess all of it. All of the side projects are just that: on the side.

In any case, these aren't conglomerates, just oligopolists aiming to be the monopolist.

05 August 2014

Live Long and Prosper Some More

Using this data set, we can see that nearly half the increase in life expectancy at birth happened before 1950. Why might that be? The introduction of penicillin, for one. Sulfa drugs for another.

Here are the decade deltas:

40 3.2

50 5.3

60 1.5

70 1.1

80 2.9

90 1.7

00 1.6

10 1.7

The total (1930 - 2010): 19.0

44% for those that are counting. If we assert that the 1970's was anomalous, and use 1.7 as its delta, then the percentage before 1950 comes in at 47%. Getting really close to half.

So, what forms of mortality remain for which we can expect new interventions to make a real differenc? Here's a graph (from the Wiki, of CDC reporting)

If it looks a bit clipped in your page, just go to the link; it's an anchor to the graphs.

The moral of the story: cure heart disease and cancer if you want to see life expectancy to move the needle. I'll not bet on it. In FDA drug approval, there's the concept of mechanism of action (MoA). The drug sponsor has to say how the drug works. For those who propound that life expectancy increase follows tomorrow as it has to today, must needs demonstrate that the MoA still persists (how the effect happens). Of course, there hasn't been just one since 1930; there's been a whole host of interventions.

As an ex-girlfriend (the only rich one, and she left me for her husband) used to say, "the one who dies with the most toys wins!" May be, but then may be not.

This missive was mostly finished, so off to get my dead trees Times and a cuppa. Should have remembered that Tuesday is Science Times day. And, of course, a piece on longevity. Not that much is new, except that it doesn't take much sweat to be beneficial. Big Pharma can't be pleased, of course. Not a lot of money to be made in life-style changes.

May be Pfizer will get a patent on running? Don't laugh. Patents on all sorts of obvious things have been granted.

Here are the decade deltas:

40 3.2

50 5.3

60 1.5

70 1.1

80 2.9

90 1.7

00 1.6

10 1.7

The total (1930 - 2010): 19.0

44% for those that are counting. If we assert that the 1970's was anomalous, and use 1.7 as its delta, then the percentage before 1950 comes in at 47%. Getting really close to half.

So, what forms of mortality remain for which we can expect new interventions to make a real differenc? Here's a graph (from the Wiki, of CDC reporting)

If it looks a bit clipped in your page, just go to the link; it's an anchor to the graphs.

The moral of the story: cure heart disease and cancer if you want to see life expectancy to move the needle. I'll not bet on it. In FDA drug approval, there's the concept of mechanism of action (MoA). The drug sponsor has to say how the drug works. For those who propound that life expectancy increase follows tomorrow as it has to today, must needs demonstrate that the MoA still persists (how the effect happens). Of course, there hasn't been just one since 1930; there's been a whole host of interventions.

As an ex-girlfriend (the only rich one, and she left me for her husband) used to say, "the one who dies with the most toys wins!" May be, but then may be not.

This missive was mostly finished, so off to get my dead trees Times and a cuppa. Should have remembered that Tuesday is Science Times day. And, of course, a piece on longevity. Not that much is new, except that it doesn't take much sweat to be beneficial. Big Pharma can't be pleased, of course. Not a lot of money to be made in life-style changes.

As a group, runners gained about three extra years of life compared with those adults who never ran.

May be Pfizer will get a patent on running? Don't laugh. Patents on all sorts of obvious things have been granted.

04 August 2014

Live Long and Prosper

The stats I was brought up on stressed that one should never, ever predict/infer beyond the range of the data. Nowadays, doing so has become far more than a cottage industry. As stressed in these pages, the only circumstance where prediction past the end of the data is (nearly) reasonable is for physical processes, which have reached stability. That is, the exogenous forces have become static.

Human processes, especially science and engineering, violate such requirements in spades. So, it was with some amusement that this post came via R-bloggers. Life expectancy changes, increase or decrease, are due to humans' ability to fool Mother Nature. It wasn't just the passage of time that life expectancy (at birth) increased by a couple of decades from the mid 1930's to today. These additional years of blessed human-hood came about as the result of improved public health, medicine, surgery, pharma and the like. Not to forget breaking the tobacco habit.

Assuming that there exist, by definition, more such interventions to move the whole of a nation's population to greater life expectancy is just stupid. No other way to say it. As it is today, new interventions are increasingly costly, and will, if not immediately then in short order, be restricted to the 1%. The needle of national life expectancy won't move even a wiggle. We've conquered the causes of widespread less-than-adult mortality. And we're not making much progress with geezer mortality. We've reached the asymptote. Too bad the quants haven't the sense to look out the window to see whether there's rain or shine.

Human processes, especially science and engineering, violate such requirements in spades. So, it was with some amusement that this post came via R-bloggers. Life expectancy changes, increase or decrease, are due to humans' ability to fool Mother Nature. It wasn't just the passage of time that life expectancy (at birth) increased by a couple of decades from the mid 1930's to today. These additional years of blessed human-hood came about as the result of improved public health, medicine, surgery, pharma and the like. Not to forget breaking the tobacco habit.

Assuming that there exist, by definition, more such interventions to move the whole of a nation's population to greater life expectancy is just stupid. No other way to say it. As it is today, new interventions are increasingly costly, and will, if not immediately then in short order, be restricted to the 1%. The needle of national life expectancy won't move even a wiggle. We've conquered the causes of widespread less-than-adult mortality. And we're not making much progress with geezer mortality. We've reached the asymptote. Too bad the quants haven't the sense to look out the window to see whether there's rain or shine.

Subscribe to:

Posts (Atom)